Searching For Clues

An ‘active’ yard is defined here as one with at least one unit (1,000+ GT) on order, and a yard is active in a specific sector if it has a ship of that type on order. The number of ‘active’ yards can be a useful indicator of shipyard capacity, with the falling number of active yards contributing to the recent decline in capacity. It should be noted that many yards are active in multiple sectors, so the total number of active yards is not equal to the sum of the yards active in each sector.

The Hound Of The Bulkervilles

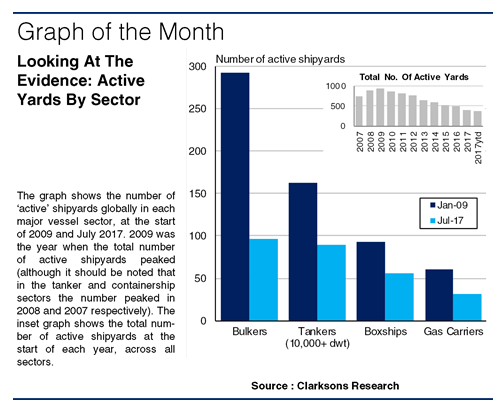

As of the start of 2009, there were 293 yards active in the bulkcarrier sector, with almost a third of total active shipyards having a bulker on order, due to the boom in bulker ordering and the relatively lower barriers to entry in the sector. This total has now fallen by 67% to stand at 97 yards. On a regional basis, the largest drop has been in China, with the number of Chinese yards with a bulker on order declining by 73% to stand at 50 at the start of July. In terms of consolidation, the ‘top 10’ yards (ranked by total dwt on order in the sector) account for 54% of the total bulker orderbook in dwt terms.

Tanker Tailor Soldier Spy

The number of active yards in the tanker sector (10,000+ dwt) on order has decreased by 55% since 2009 to currently stand at 89 shipyards, only 8 yards fewer than in the bulker sector. China, Korea and Japan each have between 10 and 20 fewer active yards in the sector. In terms of vessel types, the number of yards building crude tankers has remained steady, with the decline mainly accounted for by product and chemical tankers. Similarly to the bulker sector, the ‘top 10’ yards account for 56% of the total tanker orderbook in dwt terms.

Pandora’s Boxships

In the containership sector, the number of active yards has declined by 40% since 2009 to 56 at the start of July. The number of active Asian shipyards has dropped from 64 to 46, while the largest decline was at European yards, with only one shipyard in Europe currently building a boxship, down 96% (German yards alone accounted for 17% of the boxship orderbook in 1998 in TEU terms). Consolidation is a little stronger in the boxship sector than in the bulker and tanker sectors, with the ‘top 10’ yards accounting for 61% of the orderbook in TEU.

So, in total, there are currently 62% fewer yards ‘active’ than at the start of 2009. The largest drop has been in the bulker sector, but the number of active yards has also declined significantly elsewhere. Furthermore, 30% of currently active yards are set to complete construction of ships on their orderbook by the end of this year. With these trends in place, it will be no mystery as shipyard capacity continues to slide.

https://sin.clarksons.net/features/details/49362

")