Slower And Steadier

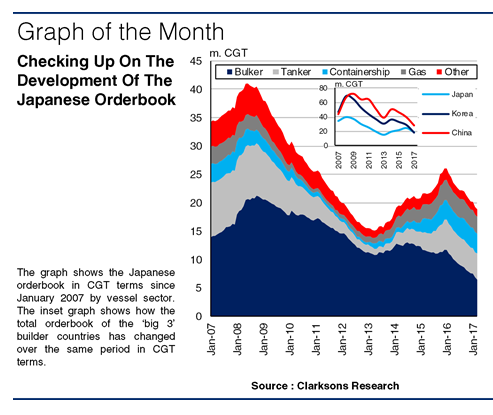

As of start March 2017, the orderbook at Japanese yards stood at 775 ships of a combined 18.9m CGT, the second largest globally. This was its lowest monthly level since January 2014 in CGT terms. However, the Japanese orderbook has experienced the smallest year-on-year decline amongst the top 3 builder nations, 23% in CGT terms compared to a 28% and 36% decline in China and Korea respectively. Furthermore, ‘forward cover’ (an indicator of future work volumes calculated by dividing the total orderbook by the previous year’s output level) at Japanese yards is currently 2.7 years in CGT terms, surpassing 2.5 years at Chinese yards and much higher than Korean yards’ 1.5 years. 59 Japanese yards currently have a ship (1,000+ GT) on order, compared to 120 Chinese yards and 16 Korean yards. The top 6 Japanese builder groups each have over 1m CGT on order and together account for around 70% of the Japanese orderbook.

Bigger Ship Benefits

In recent years, the Japanese orderbook appears to have grown more diversified. The share of bulkers on order has declined from 74% in CGT terms in March 2012 to 34% currently, while the share of tankers on order has remained steady at around 25%. Meanwhile, the share of boxships and gas carriers on order has increased from 5% in March 2011 to 34% as yards secured orders for larger ships in these sectors. 89% of boxship CGT on order is accounted for by units of 12,000+ TEU, while LNG carriers of 150,000+ cu.m. account for 83% of the gas carrier orderbook at Japanese yards. These larger units help to extend the Japanese orderbook and Japanese yards have 1.8m CGT due to be delivered in 2020 or later, compared to 0.1m CGT at Chinese yards and 0.4m CGT at Korean yards.

Home Is Where The Orders Are

Japanese yards are supported by domestic owners, with 70% of the Japanese orderbook (where ownership is known) accounted for by domestic owners in CGT terms. NYK, MOL, K-Line and their subsidiaries account for 16% of the orderbook in CGT terms. While Korean and Chinese yards also benefit from domestic ordering, Japanese yards are working with the second largest national ownership base, 163.6m GT compared to the Chinese and Korean owned fleets of 140.4m GT and 55.1m GT respectively.

So, Japanese yards are backed by a strong domestic owner base and the orderbook is becoming more diversified across the major vessel sectors, with orders for larger vessels securing a longer backlog of work. Whilst the fortunes of Japanese yards will depend on the changing shipbuilding environment, they currently have the second largest orderbook globally in CGT terms and in today’s tough newbuild contracting market, this appears to be relatively resilient.

https://sin.clarksons.net/features/details/48851